January 21, 2020

Utah State Tax Reform—What We Know Now!

But, could be on November 2020 election ballot and possibly repealed if enough signature are obtained within the allotted time frame.

- Increase in Food Sales Tax from 1.75% to 4.85%.

- New sales taxes on a wide range of services.

- Decrease in individual income tax rate from 4.95% to 4.66%.

- New Grocery Tax Credit to offset burden of this tax on low- and middle-income families.

The grocery tax credit fully phases out at 175% of the federal poverty level, so your eligibility will be determined by factoring your income in relation with your household size. For example, a family of four with an income of $45,000 will receive a full, unadjusted grocery tax credit of $500. If that same family’s income were to rise much above $45,000, the credit would begin to phase-out. Larger families may continue to receive a portion of the credit even if they are making up to $81,300 a year.

The grocery tax credit amounts to $125 a year, per person in a family of four, with an additional $50 dollars per additional child.

If you currently file a tax return, you don’t have to take any extra steps to receive the benefit of the grocery tax credit. If you make too little to pay taxes and do not currently file a tax return, contact the Department of Workforce Services, which can help you through the filing process.

The credit will come in mid-2020 (July), after the full sales tax is restored on food sales April 1. Auto distribution to tax filers. If not required to file a tax return, will need to claim the credit (not sure how at this point).

- New Utah Earned Income Credit, targeted at working families experiencing intergenerational poverty. It is designed to function in tandem with the federal earned income tax credit. In fact, Utah’s EITC is calculated off the amount provided in the federal earned income tax credit, and provides 10% of that total amount (federal EITC) to qualifying individuals and families.

For example, a single mother earning $20,000 a year, in intergenerational poverty, with two children at home, would qualify for a federal earned income tax credit of a little over $5,600. Thanks to the creation of Utah’s new EITC, she could also receive an additional $560 from the state.

The Utah Department of Workforce Services will assess eligibility for the Utah EITC. Families who have experienced poverty for more than one generation are encouraged to contact their office to determine whether or not they will be eligible for Utah’s EITC. Approximately 25,000 Utahns in intergenerational poverty are expected to qualify.

The federal tax credit is targeted to low- and middle-income households, so it gradually phases out as income increases, fully phasing out at a little over $50,000 per year for single filers with three or more children, and $56,000 for a married couple with three or more children. Smaller households will phase out at lower income levels. Utah’s EITC is based off of these numbers, but it is worth noting that the federal EITC does not have an intergenerational poverty requirement.

We encourage anyone who thinks they might qualify for this tax credit to contact the Department of Workforce Services, which will determine eligibility for the credit. They can also assist applicants in filing their federal and state tax returns.

- New Social Security tax credits for seniors.

- Increase in Utah dependent exemption amount from $565 to $2,500. In addition to dependents, joint filers with no dependent children can now receive one exemption. But a one-time rebate in spring 2020; not sure how much will come (who lost exemptions under the state’s conformity with federal tax reform in 2018). Auto distribution to tax filers of 2018 tax returns. And the dependent exemption begins to phase out for incomes over $70,000. If not required to file a tax return, will need to claim the credit (not sure how at this point). Taxpayers not see until 2021, for 2020 tax return filing.

September 18, 2018

Facts to Help You Understand IRAs

Traditional IRAs: Contributions to a traditional IRA may be tax-deductible. The amounts in a traditional IRA are not generally taxed until you take them out of the account. If you have a 401(k) or other retirement account through your employer, the amount you may contribute and deduct may be reduced or completely disallowed.

ROTH IRA: An IRA that is subject to the same rules as a traditional IRA with certain exceptions. For example, a taxpayer cannot deduct contributions to a Roth IRA. However, if the IRA owner satisfies certain requirements, qualified distributions are tax-free. Although, contributions are not deductible, the amount you may contribute may be reduced or completely disallowed if your gross income exceeds an annual limit.

Maximum Contributions: The amount of money someone puts into their IRA is subject to a dollar limit, in addition to a gross income limit.

Required Distributions: A taxpayer cannot keep retirement funds in their account indefinitely. Someone with an IRA generally must start taking withdrawals from their IRA when they reach age 70½. Roth IRAs do not require withdrawals until after the death of the owner.

Rollover: This is when the IRA owner receives a payment from a retirement plan and deposits it into a different IRA within 60 days. The best way to do this is through a direct transfer, otherwise, you may be subject tax consequences and sometimes even unnecessary tax reporting.

If you have questions, please call or email me. Don

September 13, 2018

The IRS is publishing this and I wanted to share with you:

Every day, the theft of personal and financial information puts people at risk of identity theft. Generally, thieves try to use the stolen data as quickly as possible to:

• Sell the information to other criminals.

• Withdraw money from a bank account.

• Make credit card purchases.

• File a fraudulent tax return for a refund using victims’ names.

Victims of a data loss should follow these steps to minimize the effect of the theft:

• Try to determine what information the thieves compromised. Compromised information may include emails and passwords, or more sensitive data, such as name and Social Security number.

• Take advantage of credit monitoring services when offered by the affected organization.

• Place a freeze on credit accounts to prevent access to credit records. It varies by state, but there may be a fee to place a freeze on an account. At a minimum, victims should place a fraud alert on their credit accounts by contacting one of the three major credit bureaus. A fraud alert isn’t as secure as a freeze, but it’s free.

• Reset passwords on online accounts, especially those of financial sites and email and social media accounts. Use different passwords for each account. Some experts recommend at least 10-digit passwords, mixing letters, numbers and special characters. Victims may also wish to consider using a password manager or app.

• Use multi-factor authentication, when available. Some financial institutions, email providers and social media sites allow users to set their accounts for multi-factor authentication, which requires a security code, usually sent as a text to their mobile phone, in addition to a username and password.

All taxpayers should keep a copy of their tax return. Taxpayers using a software product for the first time may need their Adjusted Gross Income amount from their prior-year tax return to verify their identity. Taxpayers can learn more about how to verify their identity and electronically sign tax returns at https://www.irs.gov/individuals/electronic-filing-pin-request Validating Your Electronically Filed Tax Return.

June 22, 2018

U.S. top court lets states force online retailers to collect sales tax

By Lawrence Hurley and April Joyner

WASHINGTON (Reuters) – States may force online retailers to collect potentially billions of dollars in sales taxes, the U.S. Supreme Court said in a major ruling on Thursday that undercut an advantage many e-commerce companies have enjoyed over brick-and-mortar rivals.

In a 5-4 ruling upholding a South Dakota law challenged by Wayfair Inc, Overstock.com Inc and Newegg Inc, the justices overturned a 1992 high court precedent that had barred states from requiring businesses with no “physical presence” there, like out-of-state online retailers, to collect sales taxes.

The ruling is likely to prompt other states to try to collect sales tax on purchases from out-of-state online businesses more aggressively. Forty-five of the 50 states impose sales taxes on purchases.

Amazon, which was not involved in the Supreme Court case, collects sales taxes on direct purchases from its site but does not typically collect taxes for merchandise sold on its platform by third-party vendors, representing about half of total sales. The ruling means that states may now seek to tax more of those sales, Moody’s analyst Charlie O’Shea said.

March 22, 2018

IRS Phone Scam Intensifies During Filing Season

As taxpayers are working to file their taxes, criminals are also hard at work — attempting to steal their money. While there are several versions of tax scams, the classic telephone con continues to thrive, especially during filing season. As a reminder, here’s how the scam works:

- Scammers call taxpayers telling them they owe taxes and face arrest if they don’t pay. Sometimes, the first call is a recording, asking taxpayers to call back to clear up a tax matter or face arrest.

- When taxpayers call back, the scammers often use threatening and hostile language. The thief claims the taxpayers may pay their debts using a gift card, other pre-paid cards or wire transfers.

- Taxpayers who comply lose their money to the scammers.

Taxpayers should remember that the IRS does not:

- Call taxpayers demanding immediate payment using a specific payment method, but will first mail a bill.

- Threaten to have taxpayers arrested for not paying taxes.

- Demand payment without giving taxpayers an opportunity to question or appeal the amount the IRS believes they owe.

- Ask for credit or debit card numbers over the phone.

Taxpayers who receive these phone calls should:

- Hang up the phone immediately, without providing any information.

- Report these calls to the:

- Treasury Inspector General for Tax Administration, using the IRS Impersonation Scam Reporting form, or by calling 800-366-4484.

- Federal Trade Commission, using the FTC Complaint Assistant on FTC.gov, being sure to include “IRS Telephone Scam” in the notes.

February 6, 2018

Employee Business Expenses & 2018 Tax Reform

Article Highlights:

- Miscellaneous Itemized Deductions Subject to the 2% AGI Floor

- Employee Business Expenses

- Employee Reimbursement Plan (Accountable Plan)

If you are an employee (i.e., a W-2 wage earner) with substantial work-related business expenses, the Act was not kind to you. It suspended (and effectively repealed), for 2018 through 2025, all miscellaneous itemized deductions, which were previously only subject to a floor of 2% of adjusted gross income (AGI). Employee business expenses are included in that category of miscellaneous itemized deductions.

EXAMPLES OF EXPENSES This change affects those who are compensated as employees and who have work-related expenses—including salespeople with travel and entertainment expenses, long-haul truck drivers with away-from-home expenses, mechanics with tool expenses, and any other employees with large but unreimbursed business expenses. These employees, beginning in 2018, will no longer be able to count such expenses as itemized deductions.

Will this change hurt you? That depends. Because employee business expenses could previously only be deducted to the extent that they exceeded 2% of AGI, the effects of the Act will depend upon the extent of your expenses. Another consideration is whether your total itemized deductions would have exceeded the new standard deduction, which has increased for 2018.

2018 WORK-AROUND As a remedy, you may want to contact your employer and try to negotiate an “accountable plan,” which is a business-expense reimbursement plan under which the employer can reimburse you, tax-free, for business expenses. With this arrangement, you would need to substantiate your business expenses to your employer and would have to return (within a specified time limit) any reimbursements that your employer pays in excess of the substantiated amount.

If you have questions related to the loss of this deduction or about how the change will impact your specific tax situation, please give this office a call.

February 2, 2018

New Tax Cuts and Jobs Act provisions.

- Personal exemptions for yourself, spouse, and dependents are no longer available.

- The standard deduction (for those not filing itemized deductions) has nearly doubled, beginning in 2018 to:

- Marrieds $24,000 ($12,700 for 2017)

- Single $12,000 ($6,350 for 2017)

- Head of Household $18,000 ($9,350 for 2017)

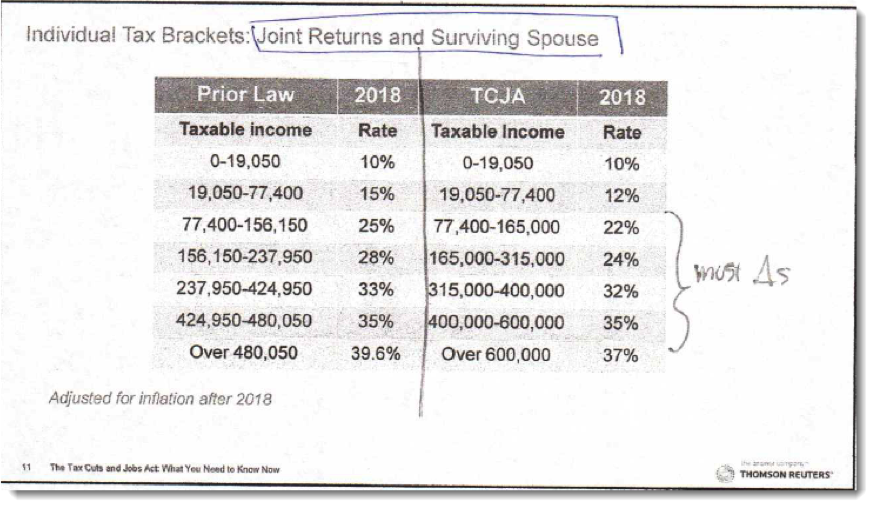

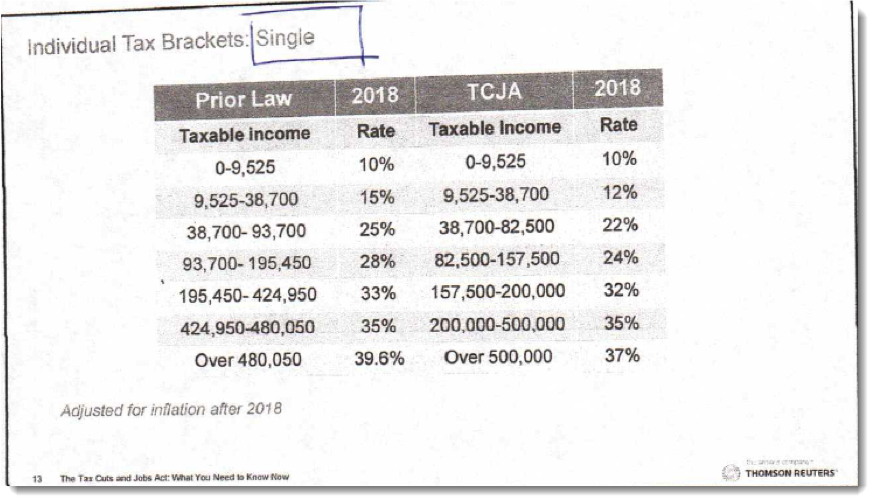

- New decreased tax rates and expanded tax-rate ranges. See the rates and ranges under prior law as well:

January, 25, 2018.

W-4 Tax Withholding for 2018

In response to the Tax Cuts and Jobs Act signed into law in December, the IRS is updating Form W-4 withholding allowances.

Per the new law, the deduction for personal and dependent exemptions are done away. Thus, withholding must reflect this and other changes, such as changes in income tax rates and the withholding tables, changes in the standard deduction, etc.

On January 11, 2018 the IRS announced that NEW WITHHOLDING tables were released to employers, which they must begin using no later than February 15th.

- But before then, employers should continue using the 2017 withholding tables.

- Employees need not do anything at this time.

Once the new 2018 W-4 is released by the IRS (not yet released as of today), I strongly urge you to revise your withholdings by submitting a new W-4 to reflect the law changes.

- The IRS will also revise their withholding calculator (a tool to help prepare Form W-4) located at https://www.irs.gov/individuals/irs-withholding-calculator.

- I can help you prepare your revised W-4 for a flat $25 fee.

- Beginning in February you should begin seeing changes to your paychecks.

WHAT IS A FORM W-4This is an IRS form that employees provide to their employers, to determine the amount of federal income tax to withhold from the employees’ paychecks. The form helps employees adjust withholding based on their personal circumstances, such as whether they have children or a spouse who is also working. The IRS always recommends employees check their withholding any time their personal or financial information changes.

January 17, 2018

2018 Game-Changers for Businesses

- Depreciation vs. Claiming a Current Deduction: Called 179: under prior law, certain fixed assets placed in services are allowed to be claimed all in the first year, rather than a deduction split up over a few years, such as furniture, business equipment, etc. Only certain assets are eligible and there is a maximum dollar amount that can be deducted this way. NEW for 2018: the maximum dollar amount substantially increased to $1 million (doubled).

- Car Deductions Have a Maximum: under prior law, vehicles may claim a depreciation deduction but because a car can be used for personal reasons, the law has a maximum amount of depreciation claimed each year. NEW for 2018: the maximum deduction for the 1st year placed in service is $10,000, $16,000 for 2nd year, $9,600 for the 3rd year, and $5,760 for 4th and later years. This is more than doubled!

- Deduction of Business Losses, called Net Operating Losses: under prior law, eligible business losses could be deducted to the extent of other income, such as wages and portfolio income. NEW for 2018: the deduction cannot 100% offset “other income” but instead only up to 80% of taxable income, but excess losses can be carried to future years, indefinitely, until used.

- New Credit for Employer Paid Family and Medical Leave: New for 2018 and 2019 only: employers may claim a credit of the amount of wages paid to qualifying employees during any period in which such employees are on family and medical leave, if the rate of payment to the employees is a minimum amount. As an employee, you may find that your employer will expand or offer this benefit!

- Business Entertainment: under prior law, business-related entertainment was deductible to the extent of 50% of the expense. NEW for 2018: entertainment expense deduction is disallowed.

NOTE: There are many other business changes, but none of them are for most of you who have small businesses.

January 9, 2018

2018 Itemized Deductions

- Medical deductions: under prior law, only medical expenses that exceed 10% of adjusted gross income are deductible. NEW for 2017 and 2018 only: the threshold is now 7½% for everyone, no matter the age.

- Overall Itemized Deduction Limitation: under prior law, high income taxpayers were limited on the amount of itemized deductions that could be claimed, called the Pease Limitation. For example, marrieds with gross income over $313,800 were subject to this reduction in itemized deductions. NEW through 2025: the limitation does not apply.

- Real Estate and Property Taxes: NEW through 2025: property taxes are limited to $10,000, and no foreign real estate property taxes are allowed.

- Mortgage Insurance Premiums (PMI): New for 2017, 2018, and forward: this deduction is not allowed.

- Mortgage Interest Deduction: under prior law, this interest is deductible on acquisition debt up to $1 million and up to $100,000 on home equity debit if the debt was incurred before December 15, 2017. The prior law also applies to mortgages with a binding contract before December 15, 2017 but the residence wasn’t purchased no later than March 31, 2018. NEW for 2018 through 2025: no longer is home equity interest deductible. The limit on acquisition debt incurred on and after December 15, 2017 is $750,000. The limits do NOT apply to refinanced debt if ONLY refinance existing debt.

- Charitable Contributions Limit: under prior law, the maximum amount you can deduct for donations to certain charities, such as churches, hospitals, and educational institutions is limited to 50% of your gross income. NEW for 2018 through 2025: the limit has increased to 60%.

- Personal Casualty and Theft Losses: under prior law, eligible taxpayers could claim a deduction if dollar thresholders were met. NEW for 2018 through 2025: these losses are not allowed, except for federally disaster losses in excess of $500. In addition, victims can withdraw retirement funds up to $100,000 early penalty free, include in income spread out over 3 years, and even repay such distributions. And, can add such losses to your standard deduction—i.e. need not itemized to claim the deduction. Or you can make a retirement loan up to $100,000 (instead of the old maximum of $50,000) and required 5-year repayment schedule can be delayed for an extra year.

- Miscellaneous Deductions: under prior law, unreimbursed employee expenses, job search expenses, investment expenses, tax preparation fees, etc. are deductible if they exceed 2% of your gross income. NEW for 2018 through 2025: these expenses are not deductible.

December 1, 2017

Debate on Tax Bill Begins: with potential changes on the horizon, here are a few suggestions for you!

- Retirement plans: If you are planning to convert a traditional IRA to a Roth IRA, do it before the end of the year. The House proposal repeals this option. Review retirement plan contributions and make sure you are contributing as many tax-free dollars you are eligible for and able to make.

- Income & Business Expenses: Review your income stream and see if there is some way to defer income to 2018 when you might be in a lower tax bracket. Make sure all your business-related expenses are in order and documented. This might be the last year unreimbursed employee business expenses are deductible.

- Itemized Deductions: Look at doubling up on itemized deductions such as property taxes, medical expenses and charitable contributions. For many taxpayers, these deductions may no longer reap the tax savings as they have in the past. While the Senate version of the tax proposal retains a deduction for real property tax, the House repealed the deduction. It might be advantageous to double up on deductions that are still allowed in 2017 and take the standard deduction in the future as both versions double the standard deduction for all taxpayers.

There would be little to no advantage this late in the tax year to close escrow now or in 2018. However, if you close in 2017, any points paid would be deductible in 2017. That deduction goes away in 2018. The small amount of mortgage interest that would be deductible in 2017 probably wouldn’t save any tax dollars and the one month of property taxes, if any, wouldn’t really make a big difference either.

Both versions of tax reform retain the deduction for charitable contributions but neither provided any detail on how taxpayers would claim a deduction. Currently charitable contributions are deducted as itemized deductions on Schedule A. If a taxpayer is no longer able to itemize because their collective deductions do not exceed the standard deduction AND charitable contributions remain an itemized deduction, it is best to make as many contributions as you can in 2017 to maximize your tax savings.

Both versions repeal the sales tax deduction. If someone is looking to maximize their itemized deductions in 2017, buying a big ticket item such as a car, boar or RV, might be appropriate. If reform passes, the deduction goes away in 2018.

November 30, 2017

IRS offers tips for 2017 year-end charitable contributions

In a news release, IRS has reminded individuals and businesses making year-end charitable contributions of several important tax law provisions, including record-keeping requirements that they should keep in mind.

Only donations to qualified organizations are tax-deductible. IRS’s “Select Check” tool is a searchable online database that lists most eligible charitable organizations; it can be found at https://www.irs.gov/charities-non-profits/exempt-organizations-select-check. Churches, synagogues, temples, mosques and government agencies are also eligible to receive deductible donations, even if they are not listed in this database.

Only taxpayers who itemize their deductions can claim deductions for charitable contributions. A taxpayer will itemize only if the total itemized deductions (mortgage interest, charitable contributions, state and local taxes, etc.) exceed the standard deduction (single $6,350, married $12,700).

To deduct any charitable donation of money, regardless of amount, a taxpayer must have a bank record or a written communication from the charity showing the name of the charity and the date and amount of the contribution. Money donations include various forms apart from cash such as check, electronic funds transfer, credit card and payroll deduction. Bank records include canceled checks, bank or credit union statements, and credit card statements, which show the

- name of the charity,

- the date, and

- the amount paid.

To be deductible, clothing and household items donated to charity must be in good used condition or better, unless a qualified appraisal is filed with the tax return. Donors must get a written acknowledgment from the charity for all gifts worth $250 or more that includes, among other things, a description of the items contributed. Special rules apply to cars, boats and other types of property donations.

Donors who get something in return for their donation (also called quid pro quo) may have to reduce their deduction. Benefits can include merchandise, meals, tickets to an event, or other goods and services. A donation acknowledgment must state whether the organization provided any goods or services in exchange for the gift along with a description and estimated value of those goods or services.

As noted above, the type of records a taxpayer needs to keep depends on the amount and type of the donation. An additional reporting form is required for many property donations, and an appraisal is often required for larger donations of property.

November 8, 2017

2018 Refund Delays Are Coming Again!

By law, the IRS cannot issue refunds for people claiming the Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) before mid-February. The law requires the IRS to hold the entire refund — even the portion not associated with EITC or ACTC.

The IRS expects the earliest EITC/ACTC related refunds to be available in taxpayer bank accounts or debit cards starting on Feb. 27, 2018, if direct deposit was used and there are no other issues with the tax return.

This additional period is due to several factors, including:

- The Presidents Day holiday

- Banking and financial systems needing time to process deposits.

- This law change, which took effect at the beginning of 2017, helps ensure that taxpayers receive the refund they’re due by giving the IRS more time to detect and prevent fraud.

As always, the IRS cautions taxpayers not to rely on getting a refund by a certain date, especially when making major purchases or paying bills. Though the IRS issues more than nine out of 10 refunds in less than 21 days, some returns require further review.

November 7, 2017

U.S. Republicans unveil tax cut bill, but the hard work awaits

U.S. House of Representatives Republicans unveiled long-delayed legislation on Thursday to deliver deep tax cuts.

The 429-page bill, representing what would be the largest overhaul of the U.S. tax system since the 1980s, called for:

- Slashing the corporate tax rate to 20 percent from 35 percent,

- Cutting tax rates on individuals and families and

- Ending certain tax breaks for companies and individuals.

Included provisions are rolling back deductions for state and local taxes. The bill would repeal the existing deduction for state and local income and sales taxes, and would cap the deduction for state and local property taxes at $10,000.

And cutting in half the popular mortgage interest deduction. The bill caps the interest deduction for future home purchases at $500,000 – half the current amount

The legislation phases out the estate tax and dumping the alternative minimum tax.

Trump called the bill an “important step” toward tax relief for Americans, adding in a statement, “We are just getting started, and there is much work left to do”.

The bill presented by the tax-writing House Ways and Means Committee would consolidate the current number of tax brackets to four from seven: 12 percent, 25 percent, 35 percent and 39.6 percent.

The bill’s architects avoided one showdown by deciding not to make changes to the popular tax-deferred 401(k) retirement savings program.

The bill would roughly double the standard deduction for individuals and families. But it would repeal a personal exemption of $4,050 that taxpayers can currently claim for themselves, their spouse and any dependents.

The bill would create a new family tax credit and double exemptions for estate taxes on inherited assets, while also allowing small businesses to write off loan interest.

It would create a new 10-percent tax on U.S. companies’ high-profit foreign subsidiaries, calculated on a global basis, in a move to prevent companies from moving profits overseas.

Foreign businesses operating in the United States would face a tax of up to 20 percent on payments they make overseas from their American operations.

The Ways and Means Committee will begin formal consideration of the bill next week before the full House can vote on it. It also must pass the Senate, where Republicans hold a slimmer 52-48 majority and earlier this year failed to garner enough votes to approve a major healthcare overhaul sought by Trump.

November 4, 2017

Check Your Withholding;

Checking Now Helps Avoid Surprises at Tax Time

As the end of 2017 approaches, the IRS encourages taxpayers to consider a tax withholding checkup.

Taking a closer look at the taxes being withheld now can help ensure the right amount is withheld, either for tax refund purposes or to avoid an unexpected tax bill next year.

“With only a few months left in the year, this is a good time to check on your withholding,” said IRS Commissioner John Koskinen. “How much you choose to withhold is a personal choice, but checking now can reduce the chance for a surprise tax bill when you file in 2018.”

By adjusting your Form W-4, you can ensure that you:

- Don’t pay too much tax during the year

- And you will have money upfront rather than waiting for a bigger refund after filing your tax return.

Under-withholding can lead to a tax bill as well as an additional penalty, particularly if you have:

- A second job

- Had a major life change

- Receive self-employment income

- OR a partner in a partnership

- OR shareholder in an S corporation.

If you do not want to take the time for year-end tax planning, the IRS offers several online resources to help you bring taxes paid closer to what is owed. They include:

- IRS Withholding Calculator – Online tool helps determine the correct amount of tax to withhold.

- IRS Publication 505 – Tax Withholding and Estimated Tax.

- Tax Withholding – Complete information on withholding, estimated taxes, FAQs and more.

November 2, 2017

How to Know if the Knock on Your Door is Actually Someone from the IRS

Every Halloween, children knock on doors pretending they are everything from superheroes to movie stars. Scammers, on the other hand, don’t leave their impersonations to one day. They can happen any time of the year.

People can avoid taking the bait and falling victim to a scam how and when the IRS does contact a taxpayer in person. This can help someone determine whether an individual is truly an IRS employee.

Here are eight things to know about in-person contacts from the IRS.

- The IRS initiates most contacts through regular mail delivered by the United States Postal Service.

- There are special circumstances when the IRS will come to a home or business, including when a taxpayer an overdue tax bill, needs a delinquent tax return, and as part of a criminal investigation.

- Revenue officers are IRS employees who work cases that involve an amount owed by a taxpayer or a delinquent tax return. Generally, home or business visits are unannounced.

- IRS revenue officers carry two forms of official identification. Both forms of ID have serial numbers. Taxpayers can ask to see both IDs.

- The IRS can assign certain cases to private debt collectors. The IRS does this only after giving written notice to the taxpayer and any appointed representative. Private collection agencies will never visit a taxpayer at their home or business.

- The IRS will not ask that a taxpayer makes a payment to anyone other than the U.S. Department of the Treasury.

- IRS employees conducting audits may call taxpayers to set up appointments, but not without having first notified them by mail. Therefore, by the time the IRS visits a taxpayer at home, the taxpayer would be well aware of the audit.

- IRS criminal investigators may visit a taxpayer’s home or business unannounced while conducting an investigation. However, these are federal law enforcement agents and they will not demand any sort of payment.

Taxpayers who believe they were visited by someone impersonating the IRS can visit IRS.gov for information about how to report it.

October 14, 2017

Health Care Reporting Requirements for 2018

The IRS today announced that it will be enforcing the health care reporting requirements for tax filing season 2018 as written in the Affordable Care Act. This will be the first time the IRS will not accept tax returns that omit this information.

IRS Statement on Health Care Reporting Requirement

For the upcoming 2018 filing season, the IRS will not accept electronically filed tax returns where the taxpayer does not address the health coverage requirements of the Affordable Care Act. The IRS will not accept the electronic tax return until the taxpayer indicates whether they:

- had coverage,

- had an exemption or

- will make a shared responsibility payment.

In addition, returns filed on paper that do not address the health coverage requirements may be suspended pending the receipt of additional information and any refunds may be delayed.

To avoid refund and processing delays when filing 2017 tax returns in 2018, taxpayers should indicate whether they and everyone on their return had coverage, qualified for an exemption from the coverage requirement or are making an individual shared responsibility payment. This process reflects the requirements of the ACA and the IRS’s obligation to administer the health care law.

Taxpayers remain obligated to follow the law and pay what they may owe at the point of filing. The 2018 filing season will be the first time the IRS will not accept tax returns that omit this information. After a review of our process and discussions with the National Taxpayer Advocate, the IRS has determined identifying omissions and requiring taxpayers to provide health coverage information at the point of filing makes it easier for the taxpayer to successfully file a tax return and minimizes related refund delays.

August 14, 2017

WHAT CONGRESS AND THE PRESIDENT ARE CONSIDERING NOW—2017 TAX REFORM

Just a few highlights from the article I read that I feel you would find interesting:

- President Trump wants to cut the top tax rate to 35% (from the current 39.6%) and the House Republican Leaders want to cut it to 33%.

- To simply taxes, the President wants to shrink the number of tax brackets to 3 from 7 AND

- To double the standard deduction (currently it is $12,700 for marrieds and $6,350 for 2017).

- Many of you who currently itemized may not need to itemize, if the proposal passes.

- And could sharply reduce charitable donations and undermine home-buying—if taxpayers are no longer itemizing.

- President Trump and the Hose want to eliminate the state income tax itemized deduction. Currently, taxes paid to states are an itemized deduction.

- Trump has promised to protect the mortgage interest and charitable deductions.

- But there is discussion of lowering the cap on the mortgage interest deduction to $500,000, down from $1 million.

The White House plans to release a brief document in early- to mid-September outlining a framework for overhauling the Code.

IRS ENCOURAGES TAXPAYERS, ESPECIALLY EARNED INCOME CREDIT AND ADDITIONAL CHILD TAX CREDIT RECIPIENTS, TO REVIEW THEIR W-4 WITHHOLDING.

Have any events in your life in 2017 occurred that would warrant the filing of a new Form W-4 with your employer? Examples include:

- Change in marital status

- A bump in income that disqualifies you from the earned income credit

- Change in number of exemptions, or dependents who turn 17 in 2017.

- Early and regular withdrawals from retirements funds

- The receipt of self-employment income and NO pre-paid FICA or federal/state taxes

These are the events that could likely affect you and may present an unwelcome surprise when filing your tax return next year. Call or email me today and I can help with you with some free tax planning—remember your first one is free! What do you have to lose?

August 7, 2017

MyRAs

Do you or are you considering a myRA account (my Retirement Account)?

On July 28, 2017, the Treasury announced it will begin winding down this program—a type of government-administered Roth IRA—after it was found not to be cost effective (Americans have paid nearly $70 million to manage the program since 2014) and that demand for them has been extremely low.

It is was initially offered in 2014 as a “starter” retirement savings accounts available through employers and backed by the US government, by then-President Obama.

Currently, the program is no longer accepting new enrollments. Existing accounts remain open and accessible, and individuals can continue to manage their accounts until further notice—deposits can be made and accounts continue to earn interest. Participants are being notified of the upcoming changes and how to move them to another Roth IRA. For more information, go to www.myRA.gov.

IRS Introduces Email Option for Direct Pay and EFTPS

The IRS has announced that it is now offering an email notification option for Direct Pay and the Electronic Federal Tax Payment System (EFTPS). This new feature sends notifications to taxpayers’ personal email account about their payments. EFTPS users can receive notifications about:

- Reminder to schedule payment

- Payment has been modified or cancelled

- Payment has been processed

- Address change confirmation

For Direct Pay: taxpayers need to sign up for email updates each time they make a payment.

For EFTPS: persons and businesses can sign up one time and they’ll receive the messages each time they pay with EFTPS.

You can cancel at any time, and to protect from potential phishing scams, the email notification will NOT contain any links to websites.

July 21, 2017

2018 Increased Deduction Limitation for HSAs under a High Deductible Health Plan (HDHP)

For calendar year 2018, the limitation on deductions if $3,450 (up from $3,400 for 2017) for an individual self-only coverage. It’s $6,900 (up from $6,750 for 2017) for an individual with family coverage. Each amount is increased by $1,000 for eligible persons age 55 or older.

An HDHP is a health plan with an annual deductible that is not less than $1,350 for self-only coverage or $2,700 for family coverage, and with respect to which the annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) do not exceed $6,650 (self-only coverage or $13,300 for family coverage.

July 14, 2017

Record Keeping Rules for Charitable Contributions

The deduction for charitable contributions began way back in 1917 as a significant source of income to nonprofits and because Congress believed that private charities are more efficient than government when providing aid to the needy, i.e. feeding the poor, providing housing for the poor, etc.

According to the National Philanthropic Trusts, Americans gave $373.l25 billion in 2015, an increase of 4.1% over 2014. Charitable deductions are allowed on Schedule A, Itemized Deductions. Only donations to qualified organizations are deductible, and certain limitations apply.

Before a deduction can be claimed, you must meet record keeping requirements. The following is a summary of those records you must have:

All contributions, regardless of amount, must have one of the following:

- Bank record

- Receipt

- Payroll deduction

Contributions of ≥$250 at one time must have all of the following:

- Acknowledgement in writing from charity

- Must show amount of contribution

- Must show a description and value of goods or services received back in exchange

- Must be received by date tax return is filed

Noncash contributions:

Less than $250 contribution, must have:

- Receipt showing name of organization,

- date,

- description of item(s) donated

$250 to $500 contribution, must have:

- written acknowledgement from organization with date,

- description of item(s) donated

- any goods or services received back in exchange

$500 to $5,000 contribution, must have:

- same as above, plus

- records showing when and how acquired,

- basis of item(s) donated

Over $5,000

- same as above, plus

- an appraisal

June 7, 2017

What is a 1031 Exchange?

A 1031 exchange is a way to rollover income taxes on the sell and receipt of like-kind property used in a business or held for investment.

Gains from exchanges are generally taxable. However, no gain or loss is recognized upon exchange of property used in a trade or business or held for investment if the property received is like-kind property used in a business or held for investment.

The properties must meet 4 requirements:

- Properties must be exchanged—as opposed to selling one and buying another.

- Both properties must be used in a trade or business or held for investment.

- Properties must be like-kind.

- Both properties must be in the USA.

Certain property does not qualify, such as stock in trade, inventory (real estate dealers hold inventory), stocks, bonds, CDs, or securities, partnership interests, and personal-use property including principal residences and second homes.

May 18, 2017

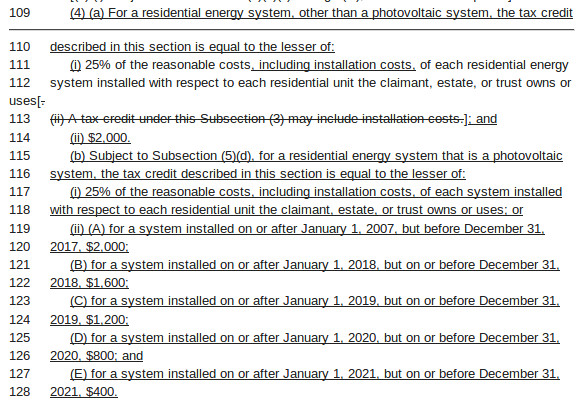

SOLAR PANELS

Herbert signed a measure into law that gradually winds down the $2,000 tax credit that homeowners can receive when they install rooftop solar panels. The credits apply to income taxes, which are the main source of funding for education in Utah. The measure from Rep. Jeremy Peterson, R-Ogden, limits the credit to $1,600 next year and scales it back every year until its $400 in 2021.

To read more go to https://le.utah.gov/~2017/bills/static/HB0023.html.

The following is a section directly from the bill:

April 27, 2017

The Trump administration has just unveiled their proposed tax overhaul with the expectation that it will be finished sometime this year. The following are the major highlights of what they are proposing:

- Cut business tax rates from a high of 35% to 15%.

- Reduce the current 7 individual tax brackets down to 3: 10%, 25%, and 35%.

- Double the standard deduction, thus for marrieds it will increase from $12,500 to $25,200.

- Repeal the AMT entirely with only one simpler tax code remaining.

- Repeal OBAMACARE NITT tax of 3.8% on higher income taxpayers.

- Reducing the top capital gain and dividend rate to 20% as a result of NITT tax repeal.

- Repeal the death tax.

- Eliminate many tax breaks and deductions, primarily for higher income taxpayers.

- But keeping homeowner and charitable tax benefits.

- Retain the child care credit and saver’s credit.

April 5, 2017

Choices for taxpayers who don’t have cash to pay their income tax bills

As the April 18th deadline for filing 2016 income tax returns draws near, practitioners may encounter some clients who don’t have cash to pay the balance due on their returns. Clients can avoid penalties but not interest if they can get an extension of time to pay from IRS. But such extensions merely postpone the day of reckoning for the period of the extension (generally, six months). This Practice Alert examines ways in which financially distressed clients may be able to defer paying their income taxes, including installment agreements and offers in compromise with IRS.

Paying in full within 120 days. A taxpayer can pay the full amount owed within 120 days, without having to pay any fee, but interest and any applicable penalties continue to accrue until the tax is paid in full. Taxpayers can use an online payment application (irs.gov/individuals/online-payment-agreement-application), or call IRS at 800-829-1040 (individuals) or 800-829-4933 (businesses).

Installment agreements. Taxpayers unable to pay the full amount owed within 120 days may be able to enter into an installment agreement with IRS to pay the tax. Apply using Form 9465, Installment Agreement Request, and Form 433-F, Collection Information Statement. (irs.gov/individuals/payment-plans-installment-agreements)

There are different rules for taxpayers who owe $10,000 or less, and for taxpayers who owe $50,000 or less.

Taxpayers are eligible for a guaranteed installment agreement ”in other words, IRS is required to enter into the agreement” if the aggregate amount of the liability (determined without regard to interest, penalties, additions to the tax, and additional amounts) is not more than $10,000 and:

- During the past five tax years, the taxpayer (and spouse if filing a joint return) have timely filed all income tax returns and paid any income tax due, and have not entered into an installment agreement for payment of income tax;

- The taxpayer agrees to pay the full amount owed within three years and to comply with all Code provisions while the agreement is in effect; and

- The taxpayer is financially unable to pay the liability in full when due and submits information that IRS may require to make this determination (i.e., a financial statement). (Code Sec. 6159(c)(2); Reg. § 301.6159-1(c)(1))

There’s a streamlined procedure for granting agreements for payment of tax in installments for amounts of $50,000 or less. IRS may accept streamlined installment agreements without requiring financial statements if

- The taxpayer owes $50,000 or less in combined tax, assessed penalties and interest,

- Has filed all returns, and

- Will pay up within 72 months, or will pay in full before expiration of the collection statue of limitations, whichever comes first. (IRM 5.14.5.2, irs.gov/individuals/online-payment-agreement-application)

Under recently finalized regs, the following fees apply to installment agreements entered into on or after Jan. 1, 2017, except for low-income taxpayers:

- $225 for regular installment agreements, where a taxpayer contacts IRS in person, by phone, or by mail and sets up an agreement to make manual payments over a period of time either by mailing a check or electronically through the Electronic Federal Tax Payment System (EFTPS). (Reg. § 300.1(b))

- $107 for direct debit installment agreements, where a taxpayer contacts IRS by phone or mail and sets up an agreement to make automatic payments over a period of time through a direct debit from a bank account. (Reg. § 300.1(b)(1))

- $149 for online payment agreements, where a taxpayer sets up an installment agreement Online Payment Agreement application on irs.gov and agrees to make manual payments over a period of time either by mailing a check or electronically through the EFTPS. (Reg. § 300.1(b)(2))

- $31 for direct debit online payment agreements, where a taxpayer sets up an installment agreement Online Payment Agreement application on irs.gov and agrees to make automatic payments over a period of time through a direct debit from a bank account. (Reg. § 300.1(b)(2))

The fee is $43 for certain qualifying low-income taxpayers, but is reduced to $31 when the taxpayer pays by way of a direct debit from the taxpayer’s bank account with respect to online payment agreements. (Reg. § 300.1(b)(3))

Offer in compromise (OIC). An OIC is an agreement between a taxpayer and IRS that settles the taxpayer’s tax liabilities for less than the full amount owed. Taxpayers who can fully pay the liabilities through an installment agreement or other means, won’t qualify for an OIC in most cases. IRS says that to qualify for an OIC, the taxpayer must have filed all tax returns, made all required estimated tax payments for the current year, and made all required federal tax deposits for the current quarter if the taxpayer is a business owner with employees. (irs.gov/taxtopics/tc204.html)

IRS may compromise a tax liability on any of the following grounds:

- Doubt as to liability. There must be a genuine dispute as to the existence of amount of the correct tax debt.

- Doubt as to collectibility. Such doubt exists in any case where the taxpayer’s assets and income are less than the full amount of the tax liability.

- To promote effective tax administration. An offer may be accepted on this ground if:

- Collection in full of the tax owed could be achieved, but

- Requiring payment in full would either create an economic hardship, or would be unfair and inequitable because of exceptional circumstances. (Reg. § 301.7122-1(b))

To request an OIC, the taxpayer must apply via Form 656, Offer in Compromise. He also must submit Form 433-A (OIC), Collection Information Statement for Wage Earners and Self-Employed Individuals, and/or Form 433-B (OIC), Collection Information Statement for Businesses. A taxpayer submitting an OIC based on doubt as to liability must file a Form 656-L (PDF), Offer in Compromise (Doubt as to Liability), instead of Form 656 and Form 433-A (OIC) and/or Form 433-B (OIC). The OIC application generally must be accompanied by a $186 application fee. However, the fee is waived for certain low income taxpayers, or if the OIC is based on doubt as to liability. (Form 656-B, Notice 2006-68, 2006-31 IRB 105, Sec. 4.03)

Except with regard to offers filed by low-income taxpayers, or based only on doubt as to liability, an OIC must be accompanied by a nonrefundable payment that depends on how the taxpayer is offering to pay.

- A taxpayer may propose to pay in a lump sum, i.e., an offer payable in five or fewer installments within five or fewer months after the offer is accepted. If such an offer is made, the taxpayer must include with the Form 656 a payment equal to 20% of the offer amount. This payment is required in addition to the $186 application fee.

- A taxpayer may propose to make periodic payments, i.e., six or more monthly installments made within 24 months after the offer is accepted. When submitting a periodic payment offer, the taxpayer must include the first proposed installment payment along with the Form 656. This payment also is required in addition to the $186 application fee. (Code Sec. 7122(c)(1))

Temporarily delay the collection process. One final option, if payment would create financial hardship, is to ask IRS to delay collection until the taxpayer is able to pay. If IRS determines that the taxpayer cannot pay any of his or her tax debt, it may report the taxpayer’s account as currently not collectible and temporarily delay collection until the taxpayer’s financial condition improves. Interest and penalties continue to accrue until the tax debt is paid in full. (irs.gov/businesses/small-businesses-self-employed/temporarily-delay-the-collection-process)

The taxpayer may be asked to complete a Collection Information Statement (Form 433-F, Form 433-A or Form 433-B) and provide proof of financial status (this may include information about assets and monthly income and expenses). During a temporary delay, IRS will again review the taxpayer’s ability to pay, and may also file a Notice of Federal Tax Lien to protect the government’s interest in his assets. To request a temporary delay of the collection process or to discuss other payment options, contact IRS at 1-800-829-1040 (individuals) or 1-800-829-4233 (businesses).

. . . . . . . . . .

What are your chances of being audited? IRS’s 2016 data book provides some clues

IR 2017-69; 2016 Data Book, irs.gov/pub/irs-soi/16databk.pdf

IRS has issued its annual data book which provides statistical data on activities conducted by IRS from Oct. 1, 2015, to Sept. 30, 2016, including on returns filed, taxes collected, enforcement, taxpayer assistance, and IRS’s budget and workforce. In addition, the data book provides valuable information about how many tax returns IRS examines (audits) and what categories of returns IRS is focusing resources on, as well as data on other enforcement activities such as collections.

During Fiscal Year (FY) 2016, IRS collected more than $3.3 trillion in revenue and processed over 244.2 million returns and supplemental documents. More than 168.8 million returns and other forms were filed electronically, representing 69.1% of all filings—an increase of 1.9% over the share of electronic filing in FY 2015. Of the nearly 149 million individual income tax returns filed, 131 million were electronically filed. More than 120 million individual income tax return filers received a tax refund, which totaled over $366.6 billion. On average, IRS spent 35 cents to collect $100 in tax revenue during the fiscal year.

What are the chances of being audited? During FY 2016, IRS examined 0.6% of all returns filed in Calendar Year (CY) 2015, about 0.7% of all individual income tax returns filed in CY 2015, and 1.1% of corporation income tax returns (excluding S corporation returns). Overall, in FY 2016, individual income tax returns in higher adjusted gross income (AGI) classes were more likely to be examined than returns in lower AGI classes.

Of the 1,034,955 individual income tax returns audited in FY 2016, roughly 36.7% (380,260) were selected for examination on the basis of an earned income tax credit (EITC) claim. Only 23.6% of the individual audits were conducted by revenue agents, tax compliance officers, tax examiners and revenue officer examiners. The 76.4% balance of the audits were correspondence audits. The following are selected audit rates:

- For business returns (for individuals not claiming the EITC and for other than farm returns) showing total gross receipts of $100,000 to $200,000, 2.2% of returns were audited in FY 2016, down from 2.5% in FY 2015.

- For business returns (for individuals not claiming the EITC and for other than farm returns) showing total gross receipts of $200,000 or more, 1.9% of returns were audited in FY 2016, a decrease from 2% in FY 2015.

- Of the returns showing farm (Schedule F) income, 0.4% were audited in FY 2016 versus 0.3% in FY 2015.

- For nonbusiness returns showing total positive income of $200,000 to $1 million, 1% of returns were audited (down from 1.8% for the previous year); for business returns, 2.3% of such returns were audited (down from 2.9% for the previous year). In general, total positive income is the sum of all positive amounts shown for the various sources of income reported on the individual income tax return and, thus, excludes losses.

- For FY 2016, the audit rate for returns with total positive income of $1 million or more was 5.8%, down from the 9.6% rate for FY 2015.

For all corporate returns (other than Form 1120-S), the audit rate in 2016 was 1.1% (down from 1.3% in the previous year). For small corporations with balance sheet returns showing total assets of: $250,000 to $1 million, the rate was 1%; for $1 to $5 million, the rate was 1%; and for $5 to 10 million, the rate was 1.6%. For FY 2015, the percentages were, respectively, 1.2%; 1.1%; and 1.5%.

For large corporations with returns showing total assets of: $10 to $50 million, the audit rate was 4.7%; for $50 to $100 million, the rate was 10.3%; for $100 to $250 million, the rate was 11.1%; for $250 to $500 million the rate was 12.2%; for $500 million to $1 billion, the rate was 13.9%; for $1 billion to $5 billion, the rate was 19.5%; for $5 billion to $20 billion, the rate was 35.7%; and for $20 billion or more, the rate was 78%. For FY 2015, the percentages were, respectively, 5.8%; 11.3%; 14.2%; 14%; 17%; 23.6%; 36.1%; and 64%.

March 22, 2017

2017 Health Care Reform: House Republicans issue Manager’s Amendment to American Health Care Act

The American Health Care Act

As anticipated, House Republicans have released a Manager’s Amendment to the American Health Care Act (AHCA), the plan to repeal and replace the Affordable Care Act (ACA, Obamacare). Although the amendment makes a number of substantive changes to the AHCA, such as accelerating the repeal of certain Obamacare taxes and lowering the floor for medical expense deductions to 5.8%, it remains uncertain whether the legislation will have sufficient support to pass the House.

What’s changed? The Manager’s Amendment includes the following changes to the AHCA’s repeal of the ACA:

- It accelerates the repeal of the 3.8% net investment income tax (NIIT) under Code Sec. 1411 to 2017.

- It accelerates the repeal of the 0.9% additional Medicare tax under Code Sec. 3101(b)(2) to 2017, and includes a transition rule to accommodate employer withholding.

- It lowers the floor for medical expenses deductions under Code Sec. 213(a) to 5.8% and accelerates this relief to 2017.

- It accelerates the repeal of the limitation on health Flexible Spending Account (FSA) contributions to 2017.

- It delays the implementation of the so-called “Cadillac” tax on high cost employer-sponsored health plans under Code Sec. 4980I to 2026.

- It accelerates the repeal of the exclusion from “qualified medical expenses” of over-the-counter medications for purposes of Health Savings Accounts (HSAs, Code Sec. 223(d)(2)), Archer Medical Savings Accounts (Archer MSAs, Code Sec. 220(d)(2)(A)), Health Flexible Spending Arrangements (Health FSAs), and Health Reimbursement Arrangements (HRAs, Code Sec. 106(f)), to 2017.

- It accelerates the repeal of the ACA’s increase to the additional tax on HSAs (Code Sec. 223(f)(4)(A)) and Archer MSAs (Code Sec. 220(f)(4)(A)) for distributions not used for qualified medical expenses to 2017.

- It accelerates the repeal of the annual fee imposed on branded prescription drug sales (ACA Sec. 9008) to 2017.

- It accelerates the repeal of the medical device excise tax under Code Sec. 4191 to 2017.

- It accelerates the repeal of the annual fee on health insurance providers (ACA Sec. 9010) to 2017.

- It accelerates the repeal of the elimination of a deduction for expenses allocable to Medicare Part D subsidy under Code Sec. 139A to 2017.

- It accelerates the repeal of the 10% tanning tax under Code Sec. 5000B to June 30, 2017.

- It accelerates the repeal of the disallowance under Code Sec. 162(m)(6) of any deduction for “applicable individual remuneration” in excess of $500,000 paid to an applicable individual by certain health insurers to 2017.

March 10, 2017 House Committees approve American Health Care Act

Following nearly 18 hours of debate, the American Health Care Act (AHCA) was approved by the Ways and Means Committee on Thursday, March 9th, by a 23-16 party line vote. The legislation would repeal the individual mandate and most Obamacare taxes, introduce a new system of age-based tax credits, and overhaul Medicaid. (See for more details.) The Ways and Means Committee, which was looking at the tax-related provisions of the bill, made no changes despite dozens of attempts by Democrats to introduce amendments.

As reported by Reuters, Republicans, who control the House and the Senate, are eyeing mid-April for passage of the bill. However, Democratic lawmakers, hospitals, and insurers have concerns about its unknown costs and impact on coverage. Notably, the bill was considered by the Committee without analysis from the nonpartisan Congressional Budget Office (CBO), although Committee Chairman Kevin Brady (R-TX) has indicated that CBO’s scoring would be available next week in advance of a House vote. Additionally, Republican lawmakers face resistance from within their own ranks by those who say the bill, which would create a system of tax credits to encourage people to buy private insurance on the open market, is not conservative enough, and some of them pejoratively refer to it as “Obamacare-lite”.

The House Energy and Commerce Committee also began marking up its portion of the bill on March 8th. The Committee resumed considering on March 9th and, after 24 hours of debate, approved the measure by a 31-23 margin.

Both parts of the legislation will now go to the House Budget Committee, which is expected to assemble the final bill which will then be voted on by the full chamber.

Draft Republican bill would replace Obamacare and include age – based health insurance credit

Draft budget reconciliation bill for 2017 fiscal year (Feb. 10, 2017)

A draft reconciliation bill that was recently leaked to the press provides significant insight into the Republican strategy to repeal and replace the Affordable Care Act (ACA, or Obamacare). The bill would repeal the individual and employer mandates and the premium tax credit and enact a new health insurance coverage credit that varies depending on the age, rather than the income, of the individual. It would also repeal the 3.8% net investment income tax and the 0.9% additional Medicare surtax.

RIA observation: Back on January 13, Congress approved a budget reconciliation resolution that instructed the relevant committees – i.e., the House Committee on Ways and Means, the House Energy and Commerce Committee, the Senate Finance Committee, and the Senate Committee on Health, Education, Labor, and Pensions – to come up with legislation by Jan. 27 to repeal the ACA. The effect of this measure was to reduce the necessary Senate votes from 60 to 51 to approve the repeal legislation. This draft bill may well have originated from one of these committees, but there is no indication at this point which committee(s) or politician(s) wrote it or how much support it has. In addition, as the draft is dated February 10th, it may not represent the most recent Republican consensus and any final version, if issued, may contain changes.

ACA repeal. The draft legislation (cited as “Bill Sec”. throughout) would repeal virtually all of the ACA, including the following tax provisions:

- The individual mandate under Code Sec. 5000A – by making the penalty amounts zero, effective for months beginning after Dec. 31, 2015. (Bill Sec. 205)

- The employer mandate under Code Sec. 4980H – by reducing the penalty amounts to zero, effective for months beginning after Dec. 31, 2015. (Bill Sec. 206)

- The premium tax credit under Code Sec. 36B would be repealed for tax years beginning after Dec. 31, 2019, and would be modified for prior years by, among other things, removing the repayment limits for excess advance payments, and modifying the applicable percentage tables in Code Sec. 36B(b)(3) (which essentially determine a taxpayer’s eligibility for the premium tax credit based on the percentage of income that the cost of health insurance premiums represents, for taxpayers with household incomes of 100% to 400% of the federal poverty line) to also take into account the taxpayer’s age. (Bill Secs. 201 – 203)

- The 3.8% net investment income tax (NIIT) under Code Sec. 1411, effective for tax years beginning after Dec. 31, 2016. (Bill Sec. 218)

- The 0.9% additional Medicare tax under Code Sec. 3101(b)(2), effective with respect to remuneration received after, and tax years beginning after Dec. 31, 2016. (The draft has a notation stating “[confirm this date]” at the end of the effective date provision.) (Bill Sec. 216)

- The higher floor for medical expense deductions under Code Sec. 213(a), effective for tax years beginning after Dec. 31, 2016. The 7.5% floor that was previously in place would be restored. (Bill Sec. 215)

- The small employer health insurance credit under Code Sec. 45R, effective for amounts paid or incurred in tax years after Dec. 31, 2019. (Bill Sec. 204)

- The limitation on health FSA contributions, for tax years beginning after Dec. 31, 2016. (Bill Sec. 210)

- The so-called “Cadillac” tax on high cost employer-sponsored health plans under Code Sec. 4980I, effective for tax years beginning after Dec. 31, 2019. (Bill Sec. 207)

- The exclusion from “qualified medical expenses” of over-the-counter medications, for Health Savings Account (HSA), Archer Medical Savings Account (MSA), Health Flexible Spending Arrangement (FSA), and Health Reimbursement Arrangement (HRA) purposes, effective for amounts paid, and expenses incurred, with respect to tax years beginning after Dec. 31, 2016. (Bill Sec. 208)

- The increased additional tax on HSAs and Archer MSAs for distributions not used for qualified medical expenses, effective for distributions made after Dec. 31, 2016. (Bill Sec. 209) The percentages would be reduced from 20% to 10% and 15%, respectively.

- The annual fee imposed on branded prescription drug sales, for calendar years beginning after Dec. 31, 2016 (Bill Sec. 211)

- The medical device excise tax under Code Sec. 4191, for sales after Dec. 31, 2017. (Bill Sec. 212)

- The annual fee on health insurance providers, for sales after Dec. 31, 2016. (Bill Sec. 213)

RIA observation: This fee is currently suspended for the 2017 calendar year.

- The elimination of a deduction for expenses allocable to Medicare Part D subsidy under Code Sec. 139A, effective for tax years beginning after Dec. 31, 2016. (Bill Sec. 214)

- The 10% tanning tax under Code Sec. 5000B, effective for services performed after Dec. 31, 2016. (Bill Sec. 217)

- The disallowance under Code Sec. 162(m)(6) of any deduction for “applicable individual remuneration” in excess of $500,000 paid to an applicable individual by certain health insurers, for tax years beginning after Dec. 31, 2016. (Bill Sec. 219)

- A number of provisions relating to the economic substance rules, effective for transactions entered into, and to underpayments, understatements, or refunds and credits attributable to transactions entered into, after Dec. 31, 2016, including:

- The codification of the economic substance doctrine under Code Sec. 7701(o),

- The Code Sec. 6662(b)(6) penalty for transactions lacking economic substance,

- The Code Sec. 6662(i) increased penalty for nondisclosed noneconomic substance transactions, and

- The Code Sec. 6664(c)(2) and Code Sec. 6664(d)(2) exclusions from the reasonable cause and good faith exceptions to the accuracy-related and fraud penalties for transactions lacking economic substance. (Bill Sec. 220)

Replacement. The bill would create a new Code Sec. 36C refundable tax credit for health insurance coverage. The credit would generally equal the lesser of the sum of the applicable monthly credit amounts (below) or the amount paid by the taxpayer for “eligible health insurance” for the taxpayer and qualifying family members. It would be subject to a $14,000 aggregate annual dollar limitation with respect to the taxpayer and the taxpayer’s qualifying family members, and monthly credit amounts would be taken into account only with respect to the five oldest qualifying individuals of the family.

The monthly credit amount with respect to any individual for any “eligible coverage month” (in general, a month when the individual is covered by eligible health insurance and is not eligible for “other specified coverage”, such as coverage under a group health plan or under certain governmental programs) during any tax year would be 1/12 of:

- $2,000 for an individual who has not attained age 30 as of the beginning of the tax year;

- $2,500 for an individual age 30 – 39;

- $3,000 for an individual age 40 – 49;

- $3,500 for an individual age 50 – 59; and

- $4,000 for an individual age 60 and older.

The above amounts, which are available to qualified individuals regardless of their income levels, would be subject to annual inflation adjustments.

The bill also provided special rules for, among other things, coordinating the credit with the medical expense deduction under Code Sec. 213, and calculating the credit where the taxpayer (or any qualifying family member) has a “qualified small employer health reimbursement arrangement” under Code Sec. 9831(d)(2) (see Weekly Alert ¶ 14 12/15/2016 and ¶ 22 for more details on small employer HRAs). (Bill Sec. 221(a)

The bill would also create a new Code Sec. 7529, which would direct a number of Agency heads to consult and establish a program for making payments to providers of eligible health insurance for taxpayers eligible for the new Code Sec. 36C credit. It would also create a new Code Sec. 7530, which would provide a mechanism under which “excess” credit amounts (generally, the amount, if any, by which the credit amount exceeds the amount paid for coverage) can, at the taxpayer’s request, be contributed to a designated HSA of the taxpayer. (Bill Sec. 221(b)) Reporting requirements relating to the health insurance coverage credit would be provided by new Code Sec. 6050X, and penalties for failure to meet the requirements would be added to Code Sec. 6724(d). (Bill Sec. 221(c))

The above provisions pertaining to the new health insurance coverage credit would apply to tax years beginning after Dec. 31, 2019.

In addition, the bill would add a new subsection, Code Sec. 106(h), which would require the inclusion in income of “excess coverage” under employer-provided health coverage. Essentially, a taxpayer would be required to include in gross income the amount for any month by which his or her “specified employer-provided health coverage” for that month exceeds 1/12 of the “annual limitation”, which is an amount determined by IRS to be equal to the 90th percentile of annual premiums for self-only, or other-than-self-only, coverage in 2019 (and adjusted for inflation thereafter). (Bill Sec. 222) Specific rules for computing the total amount of coverage, such as the treatment of health FSAs, as well as exceptions, are provided.

A similar provision would be added to limit the deduction of health insurance costs by self-employed individuals to the 90th percentile amount. (Code Sec. 162(l)(2)) (Bill Sec. 222)

The above provisions would be effective for tax years beginning after Dec. 31, 2019.

The bill would also:

- Increase the maximum HSA contribution limit to the sum of the amount of the deductible and out-of-pocket limitation, effective for tax years beginning after Dec. 31, 2017; (Bill Sec. 223)

- Allow both spouses to make “catch-up contributions” to the same HSA, effective for tax years beginning after Dec. 31, 2017; (Bill Sec. 225)

- Provide a special rule under which, if an HSA is established within 60 days of the date that certain medical expenses are incurred, it will be treated as having been in place for purposes of determining if the expense is a “qualifying medical expense”. (Bill Sec. 226)

RIA observation: There is a good deal of common ground between the proposals in the bill and those in the recently circulated GOP “Policy Brief” (see Weekly Alert ¶ 14 2/23/2017).

Policy brief explains how Republicans would address health coverage affordability February 2017

Obamacare Repeal and Replace: Policy Brief and Resources

It’s clear that Obamacare, more formally known as the Affordable Care Act (ACA), will be repealed by the Republican-controlled 115th Congress and replaced with a more market-based system of health coverage. A major question is how the replacement plan would help individuals without employer-subsidized insurance buy health coverage on the open market. A policy brief released late last week provides solid clues on how Republicans hope to get this done: an advanceable and refundable tax credit, and expanded health savings Accounts (HSAs).

Current premium tax credit for health insurance purchased on Exchange. Under current law, lower-income individuals who aren’t eligible for other qualifying coverage or “affordable” employer-sponsored health insurance plans that provide “minimum value” are allowed a refundable premium tax credit (known as a health care affordability tax credit or premium assistance credit) to subsidize the purchase of certain health insurance plans through a State-established American Health Benefit Exchange or through federally-facilitated Exchanges. (Code Sec. 36B)

The credit generally is payable in advance directly to the insurer on the individual’s behalf, with the taxpayer reconciling the actual credit that he is due on a timely filed return. Or, individuals can elect to purchase health insurance out-of-pocket and apply to IRS for the credit at the end of the tax year. Computing the credit involves a number of complicated steps.

Proposed universal health care tax credit. According to the policy brief, the Republican plan would create a new, advanceable, refundable tax credit, under new Code Sec 36C, to assist with the purchase of health insurance on the individual insurance market.

The credit would be available to all qualified individuals regardless of income, with older people receiving a higher credit amount than younger individuals, reflecting the higher cost of insurance for an older population. A qualified individual would be a citizen or qualified alien who is not eligible for coverage through other sources, specifically through an employer or government program. Taxpayers also would be able to receive credits for their dependents—including children up to the age of 26. However, incarcerated individuals would not be eligible for the credit.

The credit could be used to purchase any eligible plan approved by a State and sold in the individual insurance market, including catastrophic coverage. But the credit would not be available for plans that cover abortion. Additionally, if an employer does not subsidize COBRA (health care continuation) coverage, the individual could use the credit to help pay unsubsidized COBRA premiums while he or she is between jobs.

If the individual does not use the full value of the credit, he or she could deposit the excess amount into an HSA (see discussion below).

RIA observation: Although the policy brief refers to the universal health credit as being refundable, it doesn’t explain how this would be accomplished.

The ACA penalty taxes for the individual mandate and the employer mandate would be repealed immediately. To provide relief during a transition period, Americans eligible for the Obamacare subsidy would be able to use their credit for expanded options, including currently prohibited catastrophic plans. Additionally, the Obamacare subsidies would be adjusted slightly to provide additional assistance for younger eligible individuals and reduce the over-subsidization older individuals are receiving. Restrictions on federal funding for abortions would be included for the transition period.

Current HSA rules. In general, under Code Sec. 223, eligible individuals may, subject to statutory limits, make “above-the-line” deductible contributions to a HSA. Other persons (e.g., family members) also may contribute on behalf of eligible individuals, as may employers. Eligible individuals are those who are covered under a high deductible health plan (HDHP) (see below) and are not covered under any other health plan which is not a HDHP, unless the other coverage is certain permitted insurance (e.g., for worker’s comp).

For 2016 and 2017, an HDHP is a health plan with an annual deductible that is not less than $1,300 for individual coverage and $2,600 for family coverage. Maximum out-of-pocket expenses under the plan for 2016 and 2017 can’t exceed $6,550 for individual coverage and $13,100 for family coverage.

The maximum annual HSA deductible contribution is $3,350 for 2016 and $3,400 for 2017 (for family coverage, $6,750 for 2016 and 2017). The maximum HSA contribution is increased by an additional catch-up contribution amount (computed on a monthly basis) for individuals age 55 or older as of the last day of the calendar year who are not enrolled in Medicare. The catch-up contribution amount is $1,000.

Under Code Sec. 223, distributions from an HSA that are used exclusively to pay the qualified medical expenses of an eligible individual (account holder) or his or her spouse or dependents are excludable from gross income. Qualified medical expenses are unreimbursed expenses for medical care as defined under the medical expense deduction rules; medicine or drugs are qualified medical expenses only if prescribed (whether or not over-the-counter) or if insulin. Qualified medical expenses, which must be incurred after the HSA is established, don’t include insurance premiums other than premiums for qualified long-term care insurance, COBRA, and coverage while the eligible individual is receiving unemployment compensation.

Distributions not used for qualified medical expenses are subject to tax, and also are subject to an additional 20% for distributions reported on Form 8853 unless made after the individual attains age 65, dies, or becomes disabled.

IRS WON’T REJECT RETURNS THAT ARE SILENT REGARDING COMPLIANCE WITH ACA INDIVIDUAL MANDATE.

On its website and in a statement, IRS has announced that it will not reject returns for tax year 2016 that are silent on whether the taxpayer has complied with the individual mandate provisions of the Affordable Care Act (ACA). These provisions require the taxpayer to have qualifying health care coverage, qualify for an exemption, or pay a penalty. Although IRS had previously said such silent returns would be rejected, it shifted its policy to comply with a recent Presidential executive order directing agencies to minimize the ACA’s impact. IRS webpage titled Individual Shared Responsibility Provision.

Proposed HSA changes. The policy paper says Republicans want to expand the number of individuals who can use HSAs, and expand how they and their families can use HSAs. Specific proposals would:

- Allow HSA distributions to be used for “over-the-counter” health care items.

- Increase the maximum HSA contribution limit to equal the maximum out of pocket amounts allowed by law. For 2017, those amounts are $6,550 for self-only coverage and $13,100 for family coverage.

- Allow both spouses to make catch-up contributions to the same HSA. Specifically, if both spouses of a married couple are eligible for catch-up contributions and either has family coverage, the annual contribution limit that could be divided between them would include both catch-up contribution amounts. Thus, for example, they could agree that their combined catch-up contribution amount would be allocated to one spouse to be contributed to that spouse’s HSA. In other cases, as under present law, a spouse’s catch-up contribution amount would not be eligible for division between the spouses; the catch-up contribution would have to be made to the HSA of that spouse.